The Apartment Apocalypse? Unmasking the Myths of Multifamily Investing in 2024

Amid the blaring noise of information throughout 2023, there have been many conflicting perspectives regarding real estate, construction, and interest rates that make it difficult to discern the truth. This makes it challenging for most to paint a clear picture of what we can expect in the multifamily landscape in 2024. In the paragraphs to follow, we’ll take a precise look at what we’ve seen over the course of the last year and what we expect to see in the year ahead.

MULTIFAMILY REAL ESTATE IN 2023

Over the years, there has been a blatant lack of progress in closing the gap in the nationwide housing shortage that currently exceeds 3.8 million units. This deficit has persisted since 2008 and is projected to worsen, reaching 6.5 million homes by 2030. Rising interest rates, where each 1% increase renders five million fewer individuals eligible for homeownership, present a significant challenge. Despite existing product scarcity, new construction activity is declining, which further exacerbates the housing shortage.

Data from RealPage reveals permits are down 31.6%, while unit starts are down 31.5%. Rising interest rates compound the issue, making homeownership increasingly unaffordable for most Americans. Additionally, because of the historically low interest rates we saw during the COVID-19 pandemic, many individuals have locked in a rock-bottom interest rate and are unlikely to move. All in all, these factors contribute to the ongoing housing crisis.

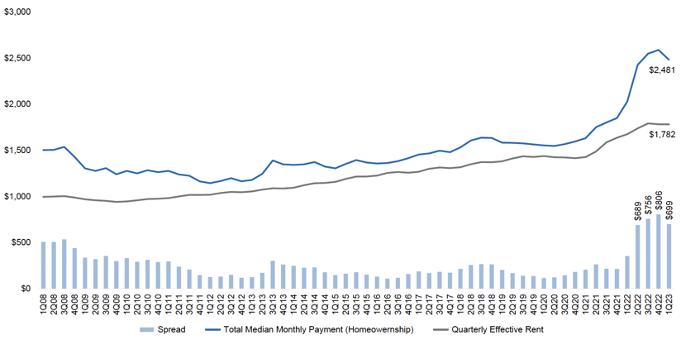

With that, current data shows that for today’s homeowner, renting is considerably more cost-effective, averaging nearly $700 less per month than owning. This significant discrepancy continues to drive the demand for rentals, as evidenced by the increasing gap depicted in the chart below.

Source: Newmark Research, Federal Reserve Bank of Atlanta, RealPage

The impact of rising interest rates has presented a double-edged sword. While it necessitates greater creativity in securing debt in the current market, it also encourages individuals to rent longer than anticipated due to affordability constraints, making it the sole option for many households.

We remain bullish in our approach to development because 18 to 30 months from now, the projects we’re funding today will open their doors — just in time for institutions to resume their multifamily investment and acquisition activity, and for our properties to welcome residents ahead of the competition.

Looking at rental rates in the market, while they have been cooling from a historic post-pandemic surge, rents are not nosediving. Rather, they are experiencing a controlled moderation following the exceptional growth of the past two years. In 2023, over ten markets still boast rental growth exceeding twenty percent according to data from CoStar.

Source: CoStar

For our investors and potential partners, understanding our conservative approach to rental growth is crucial. Industry average for rental growth historically sits around five to six percent per year. Last year, our Roers Companies portfolio achieved an eleven percent increase, exceeding this average. We believe in long-term stability and resilience. Therefore, our underwriting estimates for rental growth are significantly lower than both the national average and our own portfolio performance. We cap rental growth assumptions at three percent, ensuring a sustainable and realistic trajectory for our investments.

As we turn our attention to the future, we are actively researching and analyzing market predictions from reputable sources. This allows us to anticipate potential trends and stay ahead of the curve in the evolving rental market landscape. We can continue to make strategic decisions and deliver exceptional value for our investors. While headlines may create a sense of panic, it’s important to remember that the multifamily market is not experiencing a dramatic collapse.

2024 MARKET PREDICTIONS

While interest rates continue to be a major concern, the outlook for 2024 offers a glimmer of hope. Though economists hold varying opinions, the general consensus suggests that the cost of debt will ease up towards the second half of 2024. Economists like Doug Duncan of Fannie Mae predict a modest decline of at least 0.5 – 1% by the end of 2024. While interest rates will remain a pressing issue and a prominent topic of discussion, relief is expected to gradually emerge. Multifamily growth is also anticipated to stabilize to some degree, offering a more positive outlook for the sector.

Furthermore, the high cost of homeownership directly impacts supply, particularly in certain markets where prices have reached record levels. With construction starts anticipated to remain low in 2024, the already strong demand for rental units is expected to continue, resulting in a healthy vacancy

Construction starts — which had declined by 8.4% in 2023 — are projected to improve slightly in 2024, down by approximately 5%. This suggests a cautious resumption of construction activity, though not a dramatic surge. Construction costs are expected to continue their descent, offering significant relief to developers and investors. This trend is attributed to a surplus of materials in the market, which fosters competition among suppliers and exerts downward pressure on prices. This is already evident in the construction industry, with contractors reporting lower costs for materials and labor.

The cost reductions extend beyond construction itself, encompassing materials like windows, appliances, and doors. Roers Cos. leverages its bulk purchasing power to negotiate substantial discounts from suppliers, resulting in even greater savings on each project. These savings are then passed on to the overall project, enhancing the value proposition for investors. One recent example illustrates the magnitude of these cost reductions. Roers Cos. secured a 17% discount from a national security supplier, demonstrating the substantial savings achievable through strategic negotiations and bulk purchasing. When aggregated across multiple materials and projects, these savings become statistically significant and contribute tangibly to investor returns.

In summation, as we enter the new year, we anticipate continued improvements in construction activity and a corresponding decline in overall pricing — offering a favorable environment for developers and investors. Despite the lingering concerns regarding interest rates, leading economists predict a significant easing towards the latter half of 2024 to provide further relief. The robust demand for rental housing shows no signs of subsiding, ensuring long-term stability and growth within the multifamily sector. This sustained demand, coupled with the anticipated cost reductions, presents a compelling opportunity for investors seeking attractive returns in the real estate market.

Roers Cos. remains committed to our opportunistic approach. Our targeted strategy allows us to capitalize on the strong market fundamentals and deliver exceptional value to our investors. If you have questions about these market insights or current investment opportunities with Roers Cos., contact our investor relations team or take a closer look at the investment hub on our website: www.roerscompanies.com/investment.

SOURCES: CoStar, Fannie Mae, Newmark Research, Federal Reserve Bank of Atlanta, RealPage

Date published 12/18/2023

NO OFFER OF SECURITIES; DISCLOSURE OF INTERESTS: Under no circumstances should any material or information contained herein be used or considered as an offer to sell or a solicitation of any offer to buy an interest in any investment. Any such offer or solicitation will be made only by means of a confidential offering memorandum relating to the particular investment. Access to information about investments with projects undertaken by Roers Companies LLC, Roers Companies Project Holdings LLC, or any of their respective affiliates is limited to investors who qualify as accredited investors within the meaning of the Securities Act of 1933, as amended.

NO OFFER OF INVESTMENT, LEGAL OR TAX ADVICE. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. Prior to making any investment you should consult with a licensed investment, financial advisor, legal and tax advisor.

Current Investment Opportunities

Investment opportunities for new multifamily projects are now open.