2026 Multifamily Outlook: From Reset to Repositioning

After years of volatility, 2025 emerged as a year of recalibration for the multifamily sector. Record levels of new supply, uneven rent performance, persistent interest rate pressure, and cautious capital markets shaped operating conditions throughout the year. Importantly, this period of adjustment occurred without a broad breakdown in occupancy or renter demand, underscoring the underlying resilience of the asset class even amid peak supply pressure.

Looking ahead, research and commentary across operators, capital markets, and industry data providers point to a consistent conclusion: While market conditions are improving, the recovery will be uneven. Success will depend more on strong property management, picking the right markets, and keeping financial flexibility, rather than expecting growth across the board.

2025 in Review: Resilient Demand Amid Absorption Distortion

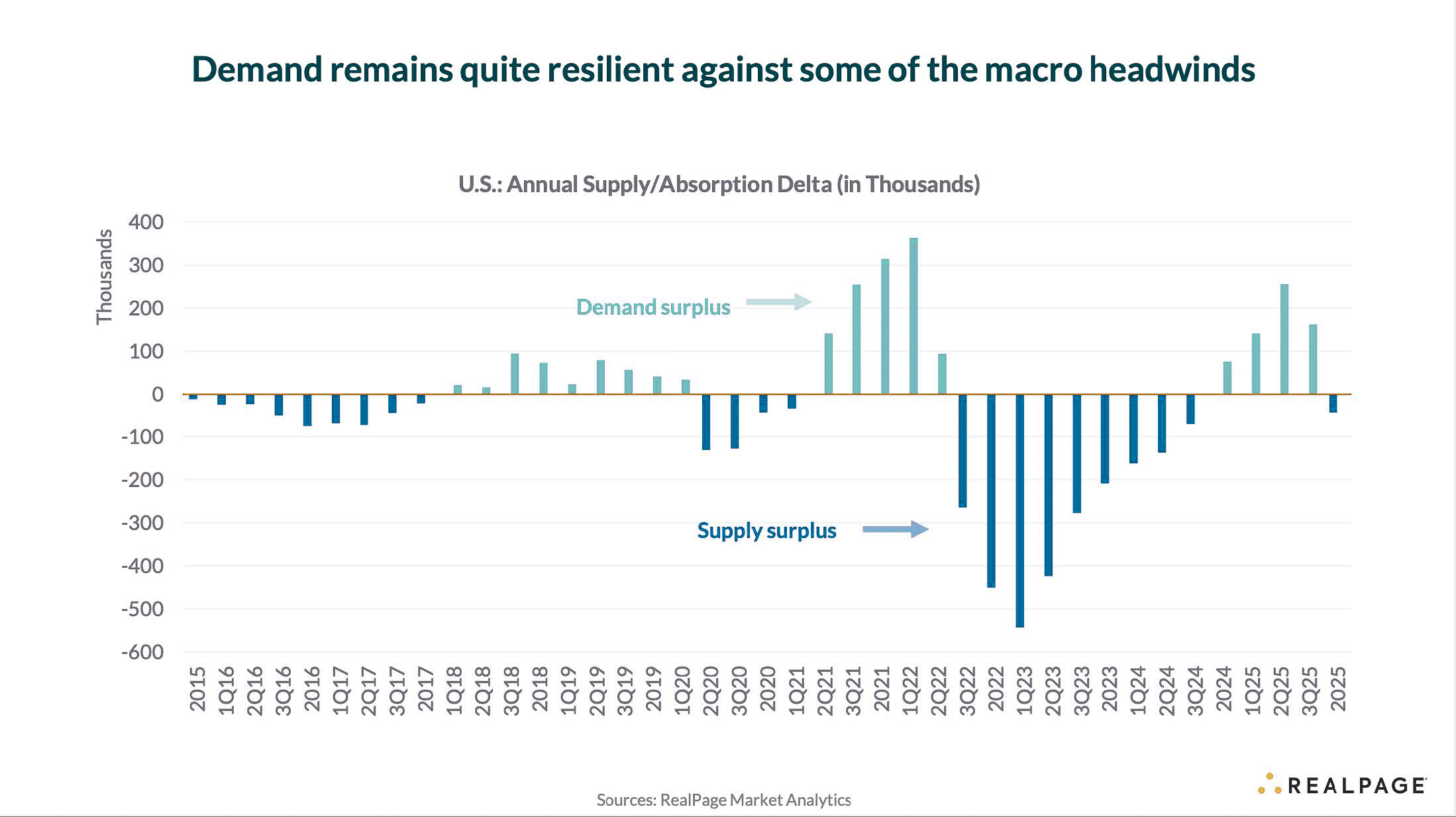

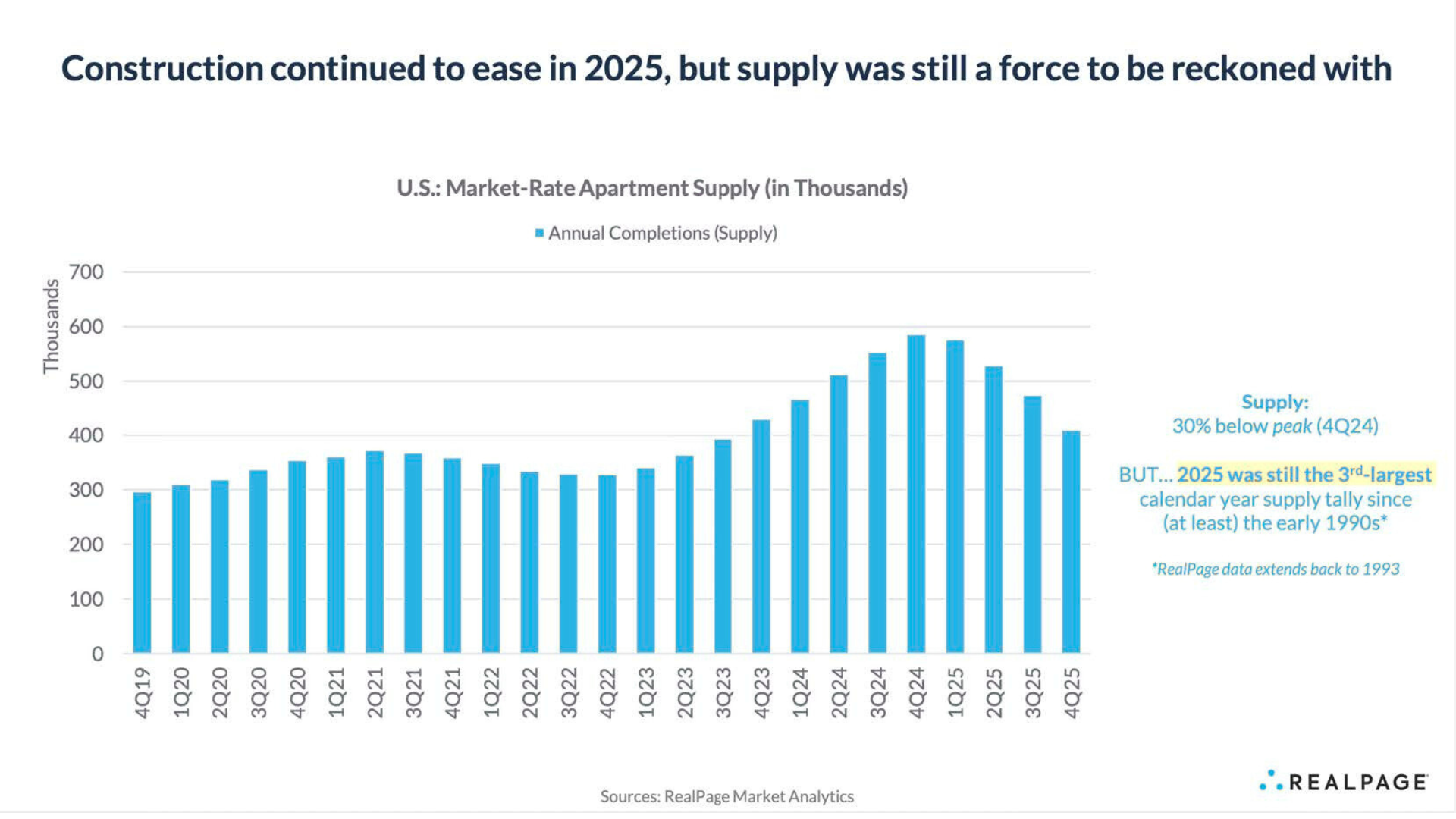

A defining story of 2025 was the collision between record multifamily supply deliveries and slower-than-anticipated absorption, setting the stage for the environment entering 2026. Many communities delivered during 2024 and 2025 were conceived in a materially different macroeconomic environment, characterized by historically low interest rates and strong housing demand. By the time these projects opened, higher mortgage rates, affordability pressure, and more cautious consumer behavior had reshaped renter decision-making.

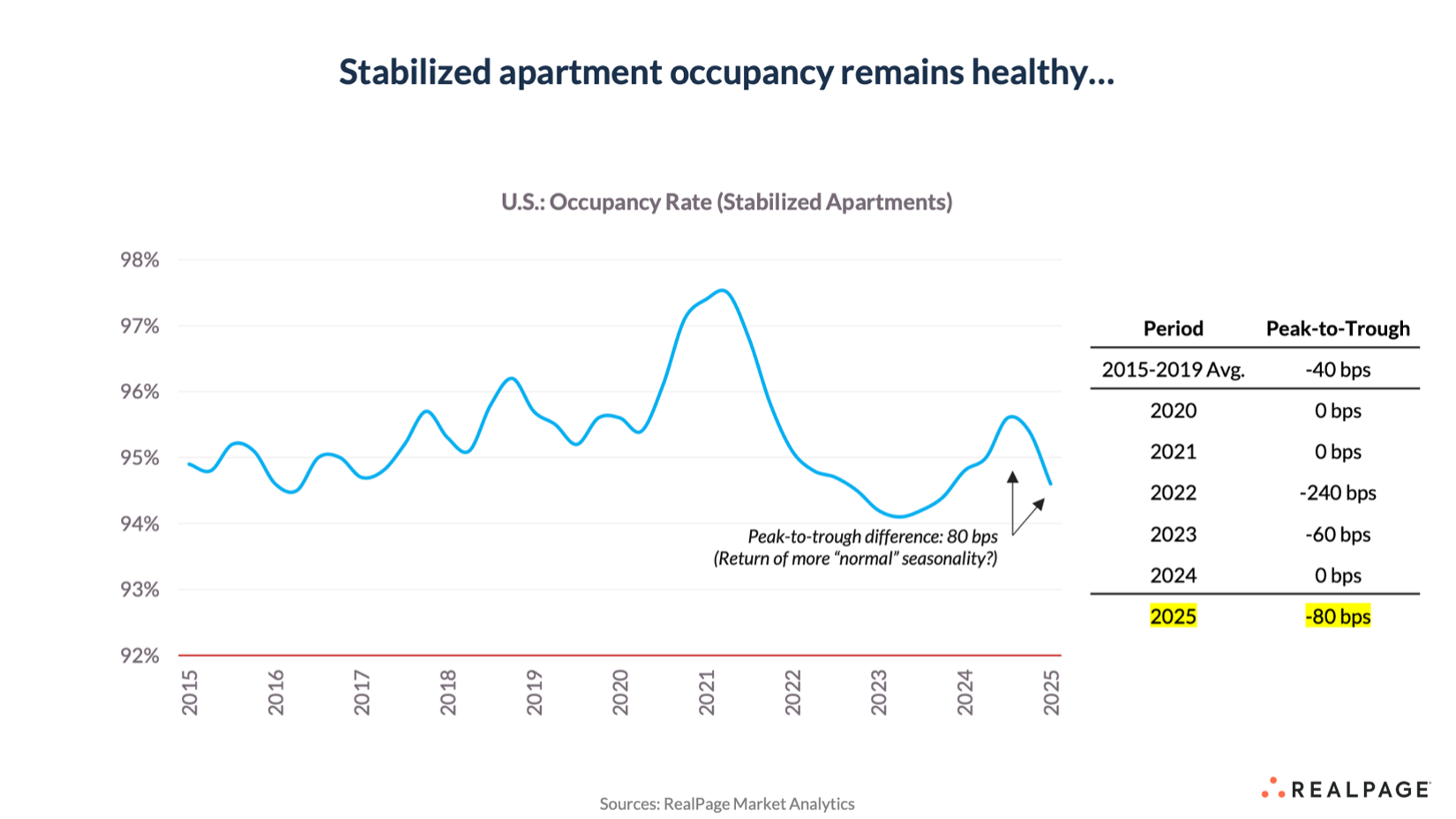

Despite these challenges, stabilized portfolio occupancy appears to have held up better than headlines often suggested. According to RealPage, stabilized occupancy remained near long-term averages, with much of the apparent softening driven by the influx of newly delivered units entering lease-up rather than deterioration in demand for existing properties.

Jay Parsons, a widely followed multifamily housing economist and industry analyst, has noted that renter demand remained resilient, but elevated new supply extended lease-up timelines in certain markets, particularly those experiencing outsized deliveries. Competitive pricing and concessions weighed on new-lease rents in select metros, while renewal rents generally proved more durable as residents opted to stay put. These dynamics created temporary pressure on revenue growth in high-supply markets, but did not necessarily signal a systemic weakening in demand.

Perhaps most importantly for investors, 2025 functioned as a stress test for the sector and reinforced a reality operators had already begun to confront. Operational execution matters more than ever. Rising insurance premiums, labor costs, utilities, and maintenance expenses placed sustained pressure on margins, pushing expense control, efficiency, and technology adoption from best practices to core operational requirements. In this environment, vertically integrated operating models, including that of Roers Cos., are positioned to manage costs more effectively, respond quickly to market shifts, and maintain consistency across the life of an asset.

The 2026 Base Case: Measured Improvement and Strategic Positioning

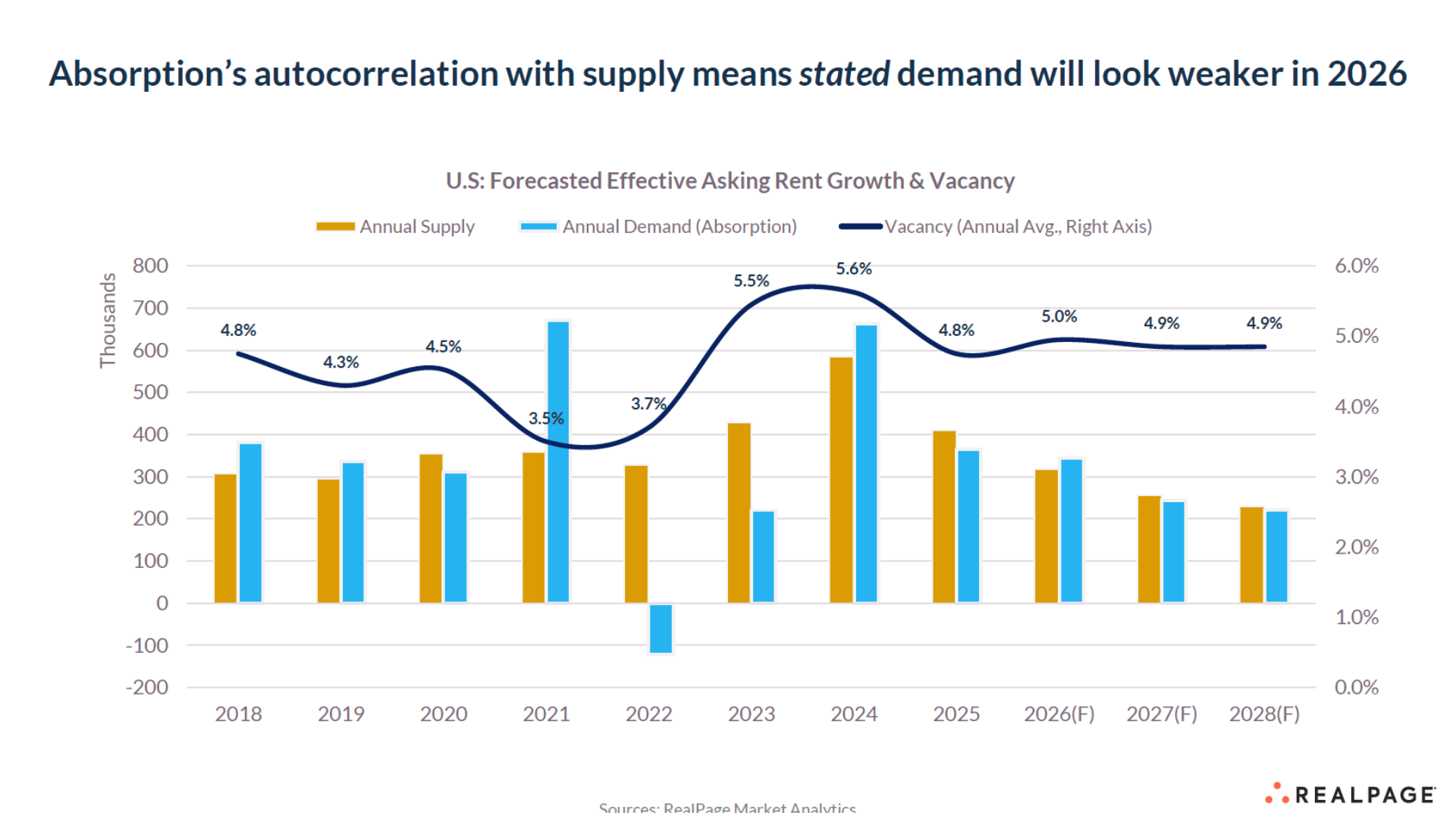

Across forecasts and industry commentary, the outlook for 2026 may be best described as measured improvement rather than a sharp rebound. RealPage data anticipates that while headline absorption is expected to decline in 2026, this may largely be a function of fewer new units being delivered rather than a pullback in renter demand. Absorption naturally correlates with available supply, and as completions slow, absorption levels are expected to normalize from the unusually high levels seen in 2024 and 2025.

This distinction is critical for investors. Lower absorption in 2026 may generate misleading headlines, but could coincide with improving occupancy, faster leasing velocity, and healthier rent growth, provided supply declines more sharply than demand. RealPage forecasts support this view, anticipating modest rent growth improvement in 2026 and predicting a more favorable setup for 2027 and beyond as supply pressure continues to ease.

This type of recovery, while less dramatic than prior upcycles, is often more durable because it is driven by normalization in supply, disciplined underwriting, and operational execution rather than speculative growth. As supply pressures ease, capital markets slowly return to normal, and execution remains a priority, operating conditions are likely to become more stable. As market conditions normalize unevenly, performance dispersion across operators and assets is expected to increase, placing greater importance on execution and asset selection.

Additional industry commentary reinforces this view. Spencer Levy of CBRE, along with recent reporting from Multifamily Dive, has observed that participants are increasingly adjusting to current pricing and interest-rate conditions following a period of heightened volatility. While transaction activity remains selective and highly market-specific, some investors and lenders appear more comfortable underwriting opportunities under today’s economic assumptions. Commentary further suggests that capital remains available in portions of the market, though deployment continues to depend on asset quality, pricing discipline, and evolving risk considerations.

Beyond near-term performance, many view 2026 as a positioning year. With development starts at cyclical lows, projects launched today are positioned to deliver into a more balanced supply–demand environment later in the cycle. Periods like this have historically rewarded patient, disciplined investors, as reduced competition and selective asset positioning often lead to stronger risk-adjusted outcomes when market conditions normalize.

Supply Finally Eases, Though Market Outcomes Will Differ

Fewer new apartment buildings are being started today than in recent years. After a prolonged period of heavy construction, many developers have pulled back, which means fewer new apartments are expected to come to market in the years ahead. This slowdown in construction is generally supportive for existing properties, as reduced new supply allows demand to catch up over time. However, the benefit is not likely to appear evenly across markets. Areas that saw significant deliveries in 2024 and 2025 may require additional time to absorb excess inventory, while markets with steadier job growth and more limited new construction are positioned to improve sooner. As a result, 2026 could be poised to reward careful market selection rather than deliver broad improvement across all locations.

In today’s more disciplined development environment, selectivity has become a defining advantage. Roers Cos. emphasizes identifying high-growth metropolitan areas and pairing them with nearby, supply-constrained suburban submarkets where housing availability has not kept pace with demand. This approach has allowed Roers Cos. to advance projects in locations where new supply is limited, competition is more manageable, and long-term fundamentals are supported as broader construction activity slows. By aligning site selection, development timing, and operational execution, Roers Cos. aims to position assets to perform through varying market cycles, particularly during periods of uneven recovery and heightened execution risk.

It is also important to distinguish between absorption and underlying market health. According to commentary by Jay Parsons, absorption levels in 2024 and 2025 reached unusually high levels largely because record supply created more units available to be absorbed. As new deliveries decline in 2026, absorption is expected to fall as well, even if renter demand remains stable. This dynamic may lead to headlines suggesting weakening demand, when in reality lower absorption could coincide with improving occupancy, faster leasing velocity, and healthier rent growth, provided supply declines more sharply than demand.

Key Fundamentals to Watch in 2026

Rent Growth and the Spring Leasing Season

Most outlooks expect rent growth in 2026 to be modestly better than in 2025, assuming new apartments are absorbed and job growth remains steady. Improvement in new-lease rents during the spring leasing season would signal that markets are stabilizing and pricing pressure is easing. If new-lease rents remain soft in high-supply markets, property performance may rely more heavily on resident retention, additional income streams, and disciplined expense management to maintain results.

Affordability Supports Ongoing Demand

Despite short-term market challenges, demand for rental housing remains supported by affordability constraints. High home prices, elevated mortgage rates, and down payment requirements continue to keep many households renting longer, helping sustain demand even during periods of slower rent growth.

Operations, Technology, and Vertical Integration as Competitive Advantages

The year 2025 demonstrated that achieving operational efficiency is critical for success in the multifamily sector. As the industry moves into 2026, companies that excel in streamlining processes, controlling expenses, and maintaining high standards of service may be better positioned to outperform. Strong operations enable property teams to respond quickly to market changes, drive consistent performance, and deliver value to residents and investors alike.

Roers Companies provides a strong example of how vertical integration supports operational excellence. By unifying development, construction, leasing, property management, and asset management under one platform, Roers Cos. achieves greater control over costs and operational outcomes. This structure facilitates faster decision-making and ensures a consistent approach throughout each stage of the project lifecycle. The company’s ability to align strategy and execution across disciplines allows it to adapt efficiently to shifting market conditions and maintain performance through various cycles.

Conclusion: a Reset, Not a Rebound

The multifamily outlook for 2026 is best described as a reset rather than a return to the easy growth of the past decade. Supply is easing, demand remains structurally sound, and capital is gradually re-engaging, but outcomes are expected to depend increasingly on execution rather than macro tailwinds.

In this environment, vertically integrated platforms like Roers Cos. appear to be well-positioned to navigate near-term volatility by focusing on controlling key cost drivers, accelerating leasing efforts, and aligning execution across disciplines. The year 2026 is likely to reward adaptability, discipline, and operational focus rather than reliance on broad market recovery alone. While the path forward may be uneven, the combination of easing supply, structurally supported demand, and improving capital market clarity provides a constructive backdrop for well-positioned operators and long-term investors.

Importantly, uneven recoveries tend to favor experienced operators and patient capital, as performance dispersion creates opportunities to differentiate rather than compete in crowded markets. The 2026 environment is less about market timing and more about execution, selectivity, and positioning capital ahead of the next supply-constrained phase of the cycle.

Click here to request the full recorded discussion and hear our team’s insights on the 2026 market outlook.

Date Published 2/4/2025

Sources

Colliers – 2026 U.S. Multifamily Outlook https://www.colliers.com/en/research/dmc-nrep-outlook-2026

Jay Parsons The Rent Roll – Episode 65 : 15 Predictions for Apartments & SFR 2026 https://www.youtube.com/watch?v=w9gDWVT8BxQ&t=3s

Multifamily Dive – 5 Multifamily Trends to Watch in 2026 https://www.multifamilydive.com/news/multifamily-transactions-distressed-sale-debt-equity/808760/

Origin Investments – Multifamily 2026 Outlook with CBRE’s Spencer Levy https://www.youtube.com/watch?v=HgLInuJjalY

RealPage – Your Guide to the 2026 Multifamily Market https://www.realpage.com/webcasts/from-data-to-decisions-multifamily-market-guide-2026/

The Gray Report – Optimism for Multifamily in 2026? https://www.youtube.com/watch?v=kv53VIeC_98

NO OFFER OF SECURITIES; DISCLOSURE OF INTERESTS. Under no circumstances should any material or information contained herein be used or considered as an offer to sell, or a solicitation of an offer to buy, any security or interest in any investment. Any such offer or solicitation, if made, will be made only by means of a confidential offering memorandum or other definitive offering documents relating to a particular investment and only in jurisdictions where permitted by law. Access to information regarding investments or projects undertaken by Roers Companies LLC, Roers Companies Project Holdings LLC, or any of their respective affiliates (collectively, “Roers”) is limited to investors who qualify as “accredited investors” within the meaning of the Securities Act of 1933, as amended. Investment outcomes vary, are speculative, and involve risk. Past performance or prior success is not indicative of, and does not guarantee, future results.

NO INVESTMENT, LEGAL OR TAX ADVICE. Nothing contained in this material is intended to constitute, and should not be construed as, legal, tax, accounting, securities or investment advice, nor as an opinion regarding the appropriateness of any investment or investment strategy for any particular person. Readers should not rely on this material in making any investment decision. Prior to making any investment, you should consult with your own licensed investment, financial, legal and tax advisors.

This material may contain forward-looking statements, including statements regarding market conditions, development activity, demand, supply, rents, interest rates, or other economic or industry trends. Such statements are based on current expectations and assumptions and are subject to risks, uncertainties and changes in circumstances, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such statements.

The information contained herein speaks only as of the date indicated and may change without notice. Neither Roers Companies LLC nor any of its affiliates undertakes any obligation to update or revise this material to reflect subsequent events or changes in circumstances.

THIRD-PARTY INFORMATION; NO REPRESENTATION AS TO ACCURACY. This material may include information, data, statistics, estimates, projections, opinions or statements derived from or based upon third-party sources believed to be reliable, including industry publications and data providers such as RealPage and similar platforms. No representation or warranty, express or implied, is made as to the accuracy, completeness or timeliness of such third-party information, and neither Roers nor any of its affiliates undertakes any obligation to verify, update or correct such information.

USE OF ARTIFICIAL INTELLIGENCE AND DATA-DRIVEN TOOLS. Certain portions of this material may have been informed by, generated with the assistance of, or incorporate outputs from artificial intelligence–enabled tools, algorithms, or data-driven platforms. AI-generated or AI-assisted content may contain errors, omissions, biases, or inaccuracies and should not be relied upon as definitive, predictive, or determinative. Any references to AI-enabled platforms are for informational purposes only and do not imply endorsement, sponsorship, or affiliation.

Current Investment Opportunities

Investment opportunities for new multifamily projects are now open.